Understanding the Life Insurance Ecosystem in Canada

The Industry Landscape in Canada

Jacob Citron

10/15/20254 min read

Today we’re getting into a high level overview of the Life Insurance ecosystem in Canada. There are millions of clients, thousands of brokers, hundreds of MGAs, and dozens of insurance companies, but what is the function of each of those things, and how do they all interact?

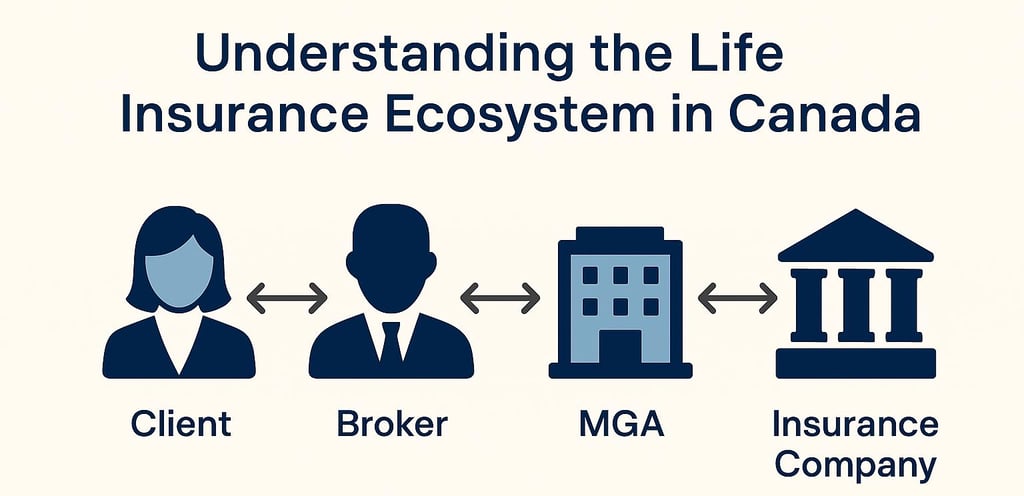

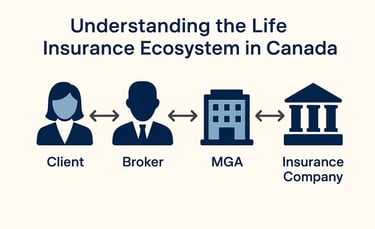

The overview - When you (The Client) work with a life insurance broker in Canada, you gain access to a wide range of life insurance companies and products. A good broker typically has contracts with multiple insurers through an intermediary called an MGA (Managing General Agency).

Here’s a simplified view of the structure:

Client ↔ Broker ↔ MGA ↔ Insurance Company

The Client

That’s you. You’re the focus and the person whose needs we aim to meet. Your role is to make decisions about offloading financial risk and put yourself in the best position possible to be navigate the unexpected. You’re here because you want to protect the things that matter most to you. You pay the premiums and, in return, receive the benefits. Whether that’s a death benefit, disability payout, or critical illness coverage.

You’ll typically work with one broker, but each broker serves many clients.

The Broker

That’s us. Our job is to understand your unique situation, goals, and risks, and then match you with the right coverage. We’re here to simplify the process as much as possible and translate “insurance language” into plain English so that it actually makes sense to the client. We’re typically paid by the insurance company, but only after you purchase a policy and pay your premium.

A good broker goes the extra mile to find the best life, disability, and critical illness insurance options for you. We maintain strong relationships with MGAs and insurers, which can sometimes lead to faster service or exceptions when needed. We spend the time on the phone with the big company, waiting on hold, finding the decision maker, so that you don’t have to. We’re also experts on personal finance, with a strong focus on tax.

Brokers can shop around on your behalf. This is one of the biggest advantages of working with a broker. Different insurers specialize in different products, so having access to multiple options helps find the best fit and price for your situation.

We also stay in touch over time, keeping up with changes in your life and staying current on industry trends, tax rules, and more. Importantly, we’re here to support you and your family through the claims process. It’s crucial to work with someone you trust to be there during difficult times, both with knowledge, and mannerism. It can also be advantageous to work with a peer or even younger, as a good broker-client relationship should last a lifetime.

The MGA

The MGA is essentially a broker for brokers. They set up contracts between brokers and insurance companies and handle many administrative tasks, like running quotes or helping navigate complex cases (for example, have you ever considered the hoops you’d have to jump through to get life insurance coverage for a professional skydiver?).

Their role is to empower brokers so that the brokers can focus on serving clients. They also remove administrative bloat for Insurance companies and act as sales distribution channels to reach markets. MGAs are paid commissions by insurance companies when a sale is made.

Each MGA works with many brokers and has contracts with multiple insurers. Likewise, each insurance company typically works with many MGAs. In some cases, some brokers will become MGAs. Buying and selling MGAs is a big part of the industry.

The Insurance Company

Insurance companies are in the business of managing risk. You pay them premiums, and in return, they take on your financial risk, whether that’s the risk of death, disability, or illness.

They receive premiums from clients and pay commissions to MGAs and brokers. The rest of the premium goes toward running their business and covering the cost of insurance.

Insurers employ underwriters to assess risk and determine pricing, and wholesalers who work directly with brokers and MGAs. You can go directly to an insurance company, but there’s no cost savings in doing so. Unlike home or auto insurance, bundling isn’t allowed in life insurance. And going direct means you lose the ability to shop around or mix and match coverage.

Reinsurance Companies

Did you know that Insurance companies have insurance? Reinsurers are the ones that insure the insurance companies (say that ten times fast). They help manage large-scale risks, like pandemics or natural disasters, that could overwhelm a single insurer’s ability to pay claims.

The Ecosystem in Sum

A good analogue to help understand it all is to think of the insurance ecosystem like you might think of Coca-Cola. The insurance company is the manufacturer, and brokers and MGAs are the stores that carry the product. The client is the one buying and drinking the soda.

Just like buying soda, you might prefer Coke over Pepsi. Some people don’t mind small differences, but others need specific features. For soda that would be diet, or cherry, for insurance that could be a policy that includes a unique rider or benefit. A broker helps you find the right "flavour" of coverage for your situation and within your price range.

Of course, you’re not expected to keep this entire ecosystem top of mind. Brokers are here to simplify it all for you, and you get that benefit at no cost. Speaking of no cost, you can reach out to Citron Insurance anytime to book a complimentary session to go over your needs or have your insurance questions answered. Remember, there is never a bad question.

Have questions but don't know where to start?

Want to get notified when our next article drops?

Subscribe: